3 Challenges Banks & NBFCs Face with CKYC Gateway Vendors

- Abhijit Shankaran

- Apr 2

- 8 min read

CKYC (Central KYC) is essential for customer onboarding and compliance. As digital lending, instant account creation, and multi-product relationships expand across banks and NBFCs, institutions need to interact with the Central Know Your Customer registry effectively, securely, and in accordance with regulatory standards.

Central KYC is a unified Know Your Customer registry managed by CERSAI under the Prevention of Money Laundering Act. Every regulated financial institution in India, such as banks, NBFCs, insurance companies, and securities firms, must search, download, and upload KYC records through this registry for all new customer onboarding.

For most institutions today, this interaction is not direct but facilitated by CKYC Gateway vendors who act as intermediaries between institutional systems and CERSAI. Although this setup initially seems convenient, it introduces deeper structural challenges that become more significant as institutions expand their operations, product lines, and regulatory exposure.

Before exploring alternatives, it's crucial to understand why the traditional vendor-led gateway model is increasingly being questioned and how CYKC ownership is evolving into a strategic decision rather than a technical one.

Understanding the Vendor-Led CKYC Gateway Model

CKYC Gateway vendors usually provide pre-built integrations with CERSAI, ensuring quick onboarding for banks and NBFCs. Core systems like CBS, LOS, LMS, cards, and insurance platforms link to the vendor, who then connects to the CKYC registry to execute search, download, upload, and update operations.

In theory, this approach minimizes initial engineering efforts. Institutions bypass the complexity of direct integration and depend on the vendor to handle protocol changes, certifications, and connectivity. Yet, this ease of use comes with a sacrifice of control, transparency, and long-term resilience.

As KYC volumes grow and regulatory expectations become stricter, institutions start to realize that CKYC routed through commercial intermediaries introduces risks that are not always apparent during the early stages of implementation.

Challenge 1: Data Sovereignty and Exposure Risk

KYC data is highly sensitive, and routing it through third‑party servers increases the risk of unauthorised access and data breaches.

A major challenge with vendor-led CKYC gateways is data sovereignty. In many cases, customer KYC data is processed and temporarily stored on the vendor’s infrastructure before being sent to CERSAI or returned to the institution.

This raises significant governance concerns. KYC data contains highly sensitive personal and identity information. Routing this data through third-party servers increases the risk of breaches, unauthorised access, and cross-border data-handling issues. For institutions subject to RBI data governance and localization requirements, justifying such architectures during audits becomes increasingly challenging.

From a risk standpoint, the institution remains fully accountable, even if a breach or exposure occurs at the vendor level. As regulatory scrutiny intensifies, CYKC data moving beyond institutional boundaries is no longer a comfortable or defensible stance.

Challenge 2: Intermediary Dependency and Loss of Control

Logging, error handling, retries, and audit trails are often hidden behind vendor dashboards

Vendor-based CKYC models create a structural dependency, preventing institutions from having direct access to CERSAI. All interactions occur through the vendor’s platform, APIs, and operational processes.

This dependency leads to several issues. Firstly, institutions lose insight into the execution of CKYC searches, downloads, uploads, and updates. Logging, error handling, retries, and audit trails are often hidden behind vendor dashboards. Secondly, contract structures often include long lock-in periods, making vendor changes costly and operationally risky.

Over time, the vendor becomes a single point of failure. Any outage, compliance issue, or pricing change directly affects frontline onboarding operations. As institutions advance digitally, this lack of autonomy over CKYC workflows becomes a hindrance rather than a benefit.

Challenge 3: The Per-Transaction Cost Trap

CKYC costs increase in direct proportion to business volume

Most CKYC gateway vendors use a transaction-based pricing model, where fees are charged for each search, download, upload, or update. This pricing structure may seem reasonable during initial growth stages, but it becomes excessively expensive as scale increases.

Banks and NBFCs that onboard thousands or millions of customers annually notice that CKYC costs increase in direct proportion to business volume. Unlike platforms owned internally, these costs do not stabilize. Each additional customer results in additional costs. Over time, CKYC transforms into a recurring operational expense rather than a one-time infrastructure investment.

For institutions rapidly expanding into retail lending, digital savings accounts, or mass-market insurance, this model gradually reduces profit margins. From a long-term planning perspective, linking such a critical compliance function to variable vendor fees makes CKYC financially inefficient.

This blog is written and SEO Optimized by Abhijit Shankaran. Content marketing specialist at SimSol Technologies.

Fragmented KYC Ecosystems Across Internal Systems

A frequent outcome of vendor-driven CKYC gateways is fragmentation. Various product lines and systems often connect with the vendor independently. Consequently, KYC data is utilized, modified, and stored in diverse formats across CBS, LOS, LMS, cards, and other platforms.

This results in data silos and version discrepancies. One system might contain an outdated KYC address while another reflects an updated version. These inconsistencies emerge as control failures during regulatory audits, even though the underlying issue stems from fragmented integration design.

When KYC data is managed externally rather than centrally governed, CYKC becomes challenging to establish as a single source of truth within the institution.

The CKYCRR 2.0 Upgrade and Its Importance

CERSAI's transition to CKYCRR 2.0 marks a major change in how institutions must connect with the CKYC registry. The old flat files have been replaced by structured API-based interactions using JSON or XML. New requirements include DSC authentication, OTP-based consent for downloads, Aadhaar masking, data localisation, and comprehensive audit trails.

For institutions relying on vendor gateways, this upgrade brings urgency and uncertainty. Banks and NBFCs must rely on vendors to update their platforms, adjust timelines, and obtain regulatory certifications. Institutions have limited influence over vendor roadmaps and minimal insight into the quality of implementation.

This upgrade cycle compels leadership teams to reconsider whether continuing with intermediaries or directly managing CYKC integration aligns better with their long-term compliance strategy.

What the CKYCRR 2.0 Upgrade Means for Institutions

The CKYCRR 2.0 framework enhances accountability standards. System-level evidence of consent, audit trails, and data handling practices are now mandatory. Institutions must be prepared to demonstrate comprehensive control over KYC processes.

For RBI-regulated entities, justifying the routing of customer KYC data through third-party commercial platforms is becoming increasingly difficult. The upgrade presents a natural decision point: either continue relying on an intermediary or invest in direct ownership of CKYC integration and governance.

In many instances, CYKC compliance strategy now aligns with enterprise risk management rather than merely technology procurement.

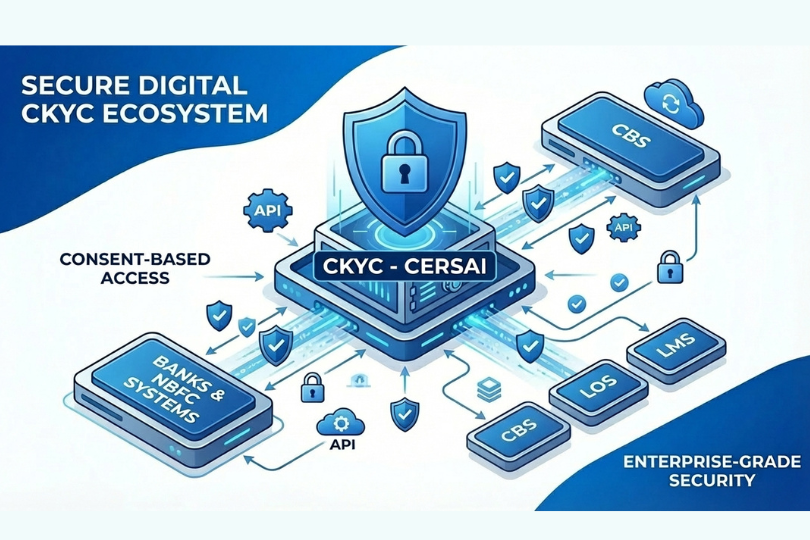

Introducing SimTrust as a Bank-Owned CKYC Gateway

SimTrust is a production-ready CKYC Gateway tailored for banks, NBFCs, cooperative banks, MFIs, insurance companies, and stockbrokers seeking to manage their own CKYC capabilities. SimTrust facilitates direct connectivity between the institution and CERSAI, eliminating the need for a vendor intermediary.

SimTrust establishes a direct connection to CERSAI’s CKYCRR 2.0 APIs using the institution’s Digital Signature Certificate. All CKYC operations, including search, download, upload, and updates, are conducted entirely within the institution’s infrastructure. No customer data is routed through SimSol’s network.

Customers do not interact with external vendor systems, and KYC operations do not pass through third-party servers. SimTrust serves as the gateway, allowing the institution to maintain full control over CYKC execution, data flow, and compliance posture.

This allows SimTrust to make financial institutions independent, with 100% control and minimal reliance on vendors.

How SimTrust Integrates Across Institutional Systems

SimTrust acts as a centralized integration hub for all internal platforms. Core banking systems, loan origination systems, loan management systems, card platforms, and other applications connect to SimTrust using standardized interfaces.

This architecture ensures that verified KYC data is consistently distributed across all systems from a single controlled source. Instead of creating multiple integrations with different vendors, institutions centralize CKYC orchestration internally. This approach significantly reduces data mismatches, manual reconciliations, and audit discrepancies.

By consolidating CKYC operations internally, CYKC becomes a governed capability rather than a fragmented service.

Built-In Compliance and Audit Readiness

SimTrust integrates regulatory requirements directly within the platform. The platform's compliance controls ensure Aadhaar masking, OTP consent verification, DSC authentication, and required audit logging are enforced.

Each CKYC transaction is recorded with user identity, timestamps, and results. Detailed reporting and audit trails are accessible, allowing institutions to confidently address supervisory inspections.

This method converts CYKC from an external compliance requirement into an internal control framework that can be audited.

Designed for Institutions of Every Size

SimTrust is perfectly suited for scheduled commercial banks, NBFCs, cooperative banks, MFIs, insurance companies, and capital market intermediaries. The platform can handle from thousands to millions of KYC records, scaling efficiently without adding variable costs per transaction.

Its key features include real-time KYC search, KYC upload and registration, record download and retrieval, multi-system integration, compliance controls, and detailed audit reporting.

By managing the gateway themselves, institutions can align CKYC capabilities with business growth instead of being tied to vendor pricing models.

Why is there a Shift Away from Vendor-Led Gateways

As regulatory expectations evolve, the acceptance of unclear third-party reliance is quickly diminishing. Institutions must comprehend, demonstrate, and justify how customer identity data moves through their systems.

Taking charge of CKYC integration signifies taking responsibility. It minimizes dependency risks, aligns with RBI data governance principles, and prepares the institution for future regulatory advancements. For leadership teams assessing long-term digital resilience, CKYC ownership is now a strategic architectural choice rather than merely a software acquisition.

Final Thoughts

CKYC Gateway vendors contributed to the rapid early adoption within the financial sector. However, as institutions expand, diversify their products, and undergo more stringent audits, the drawbacks of models led by intermediaries become apparent.

Issues such as data sovereignty risks, dependency lock-ins, increasing transaction costs, fragmented internal ecosystems, and uncertainty in upgrades accumulate over time. The CKYCRR 2.0 upgrade has highlighted these challenges, prompting a need for reassessment.

By offering direct CERSAI connectivity, internal governance, and complete operational control, SimTrust presents an alternative that aligns compliance with ownership. In a setting where trust, transparency, and accountability are crucial for operational resilience, rethinking CYKC architecture is now essential.

FAQ

What is CKYC and why is it important for banks and NBFCs?

CKYC is a centralized KYC registry managed by CERSAI that allows banks and NBFCs to use a single, verified customer KYC record across products. It reduces onboarding time, lowers operational costs, and ensures RBI-compliant customer verification.

Why is CKYC mandatory for banks and NBFCs in India?

RBI mandates CKYC under the PMLA and Master Direction on KYC. Banks and NBFCs must search, download, and upload KYC records through CERSAI to ensure standardized identity verification and prevent money laundering risks.

What challenges do banks face with traditional CKYC integrations?

Most banks rely on third-party vendors for CKYC access, leading to limited visibility, higher data exposure risk, fragmented integrations, and audit complexity. This makes governance and compliance harder to manage at scale.

What is SimTrust CKYC Gateway?

SimTrust is a bank-owned CKYC Gateway that enables direct integration with CERSAI’s CKYCRR 2.0 APIs. It allows banks and NBFCs to perform all CKYC operations within their own infrastructure without third-party data access.

How does SimTrust help banks own their CKYC capability?

SimTrust is deployed on the institution’s servers and uses the bank’s Digital Signature Certificate for all CKYC operations. This ensures full control over data, consent, audit logs, and regulatory compliance.

How does SimTrust improve CKYC compliance and audit readiness?

SimTrust automatically logs every CKYC action including search, download, upload, and update with user identity and timestamps. This creates a complete audit trail aligned with RBI and CERSAI requirements.

Is SimTrust compliant with CKYCRR 2.0 requirements?

Yes. SimTrust supports direct REST API integration, DSC-based authentication, OTP-based consent for downloads, Aadhaar masking, data localisation, and detailed audit logging as mandated under CKYCRR 2.0.

How does SimTrust integrate with bank and NBFC systems?

SimTrust acts as a central CKYC hub that connects with CBS, LOS, LMS, cards, and other internal systems. Verified KYC data is distributed securely across systems from a single source.

Does customer KYC data pass through SimTrust or SimSol servers?

No. All CKYC operations and data processing happen entirely within the institution’s infrastructure. Customer data never traverses SimSol’s network and no third-party middleware is involved.

Why should banks and NBFCs choose SimTrust over vendor-led CKYC models?

SimTrust eliminates vendor dependency, reduces data risk, improves regulatory control, and enables banks to treat CKYC as a core internal capability rather than a leased compliance service

Also Read:

What is CKYC? Why is it important?

Comments